In the last two years or so, the Australian cash rate has halved, 10-year bond yields have fallen by two thirds and interest rates have resumed falling globally. The hunt for income is a hunt indeed.

Ever-lower interest rates and periodic turmoil in investment markets provides an ongoing reminder of the importance of the income (cash) flow or yield an investment provides.

Here’s five charts I find useful in understanding investing for income:

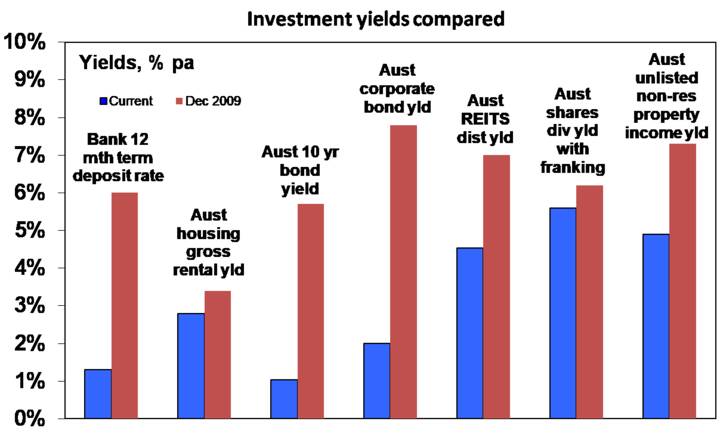

1. Alternatives to bank deposits

This chart shows the yield available on a range of investments both now and in December 2009, almost 10 years ago, for comparison.

Source: Bloomberg, REIA, RBA, JLL, AMP Capital

Key messages

First, the yield on bank deposits and government bonds is woeful. Second, there are alternatives to cash when it comes to yield or income, notably shares, property and infrastructure but even here yields have generally trended down (albeit less so for shares).

Of course, investors need to allow for risk. Bank deposits have close to zero risk, but any move to higher-yielding investments does entail taking on risk.

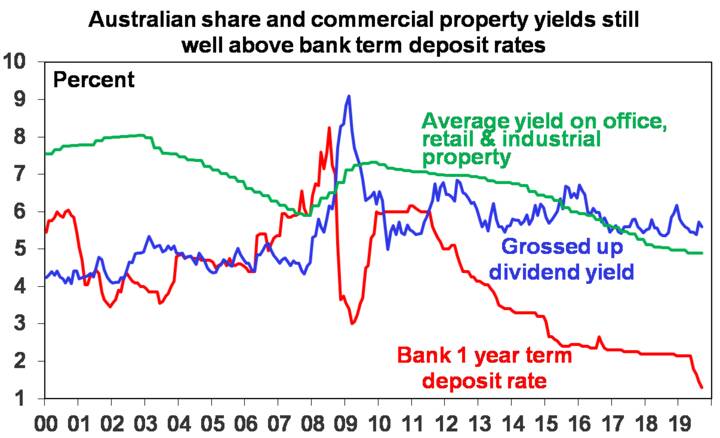

2. The gap between different yield on assets provides a guide to value

The next chart shows average yields on Australian shares and unlisted commercial property relative to the one-year term deposit rate since 2000. With share and property yields not plunging to the degree bank deposit rates have, the gap between the former and latter is extremely wide.

Source: JLL, Bloomberg, AMP Capital

Key messages

Comparing yields provides a guide to relative value, and shares and unlisted commercial property remain very attractive relative to bank deposits.

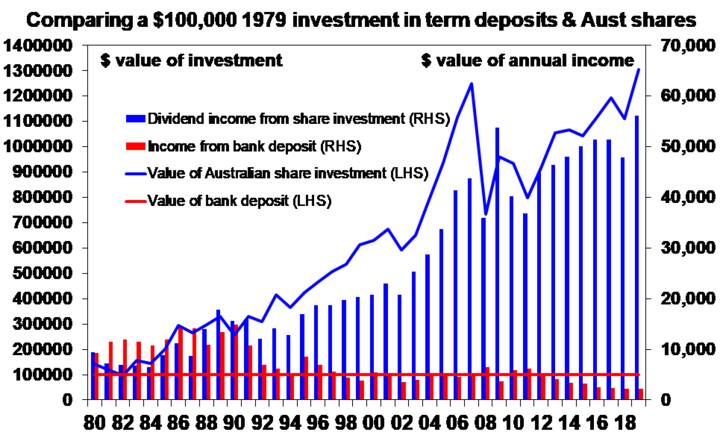

3. Shares can provide growth in income with less volatility than bank deposits

Investing in shares entails the risk of capital loss, but can offer a higher and less volatile income flow over time. The next chart compares initial $100,000 investments in Australian shares (ASX 200) and one-year term deposits in December 1979 and the income they have provided over time (before franking credits are allowed for in the case of shares.)

2019 data is year to date/annualised. Source: RBA, Bloomberg, AMP Capital

Key messages

Shares come with the risk of capital loss, but a well-diversified portfolio of Australian shares can provide stronger growth in income with less volatility in that income than bank term deposits.

The key question investors focused on income (or cash flow) need to ask is, what is more important: stability in the value of their investment or a higher, more sustainable income flow than bank deposits offer? If investors do go down the shares path, it’s critical to have a well-diversified portfolio of shares paying high and sustainable dividend yields.

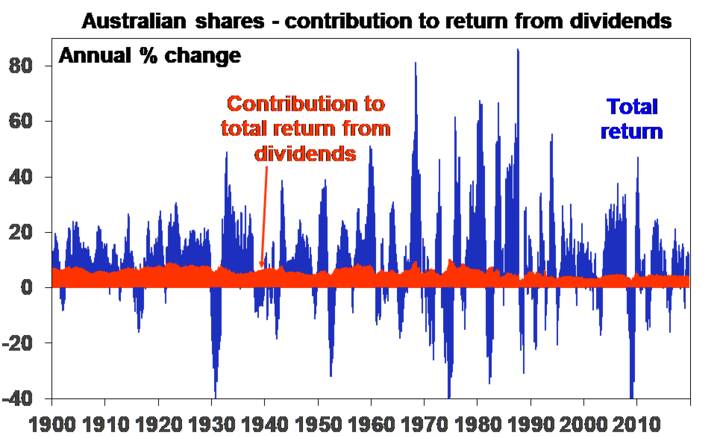

4. A bird in the hand is worth two in the bush

Since 1900, dividends (prior to allowing for franking credits) have provided just over half of the 11.8 per cent average annual return from Australian shares and as can be seen in the next chart their contribution has been stable in contrast to the capital value of shares.

Source: Global Financial Data, Bloomberg, AMP Capital

Key messages

A high and sustainable income yield for an investment provides some security during volatile times. It’s a bit like a down payment on future returns.

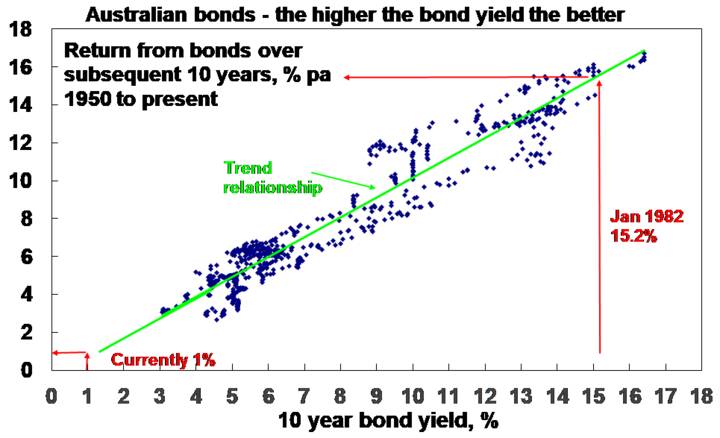

5. Yield provides a looking glass (of sorts)

The next chart, which shows a scatter plot of Australian 10-year bond yields since 1950 (along the horizontal axis) against subsequent 10-year bond returns based on the Composite All Maturities Bond Index (vertical axis).

Source: Global Financial Data, Bloomberg, AMP Capital

Key messages

While returns have been solid lately, low investment yields do warn of lower returns ahead – most notably from government bonds.